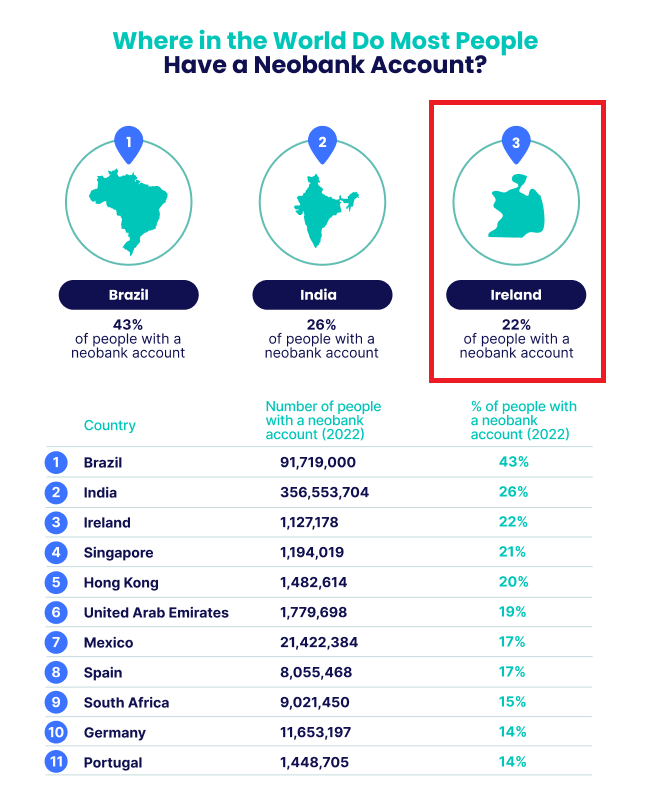

Which Countries Have Adopted Neobanks the Most?

Figure 1

Ireland - 22% of Irish people use a digital-only bank

Apparently, Ireland is one of the countries using Neobanking the most, with around 22% of Irish people using a digital-only bank according to an article appearing on the website of Seon Technologies. It goes on to say that '[a]ccording to current population estimates, around 1,127,178 residents currently use Neobanking. Finder predicts this could increase to 34% by 2027.' This is interesting because, Revolut said in July 2022 that it has 1.9million customers in Ireland.

Beating Ireland to the top spot is Brazil at #1 with 43% of the population having a Neobank account followed by India in the #2 spot with 26% of Indians using a digital-only bank.

Seon Technologies, which used data from Finder, reported that around 356,553,704 of India's populatuion could be Neobank account holders, putting them in first place as the country that uses digital banking the most. Meanwhile according to current population estimate for Braziln at 91,719,000, digitization of its economy has been accelerated by both the pandemic and popular Neobanks seeing their client base grow exponentially (a bit of a cause and effect observation). Brazil is also home to Latin America’s biggest Neobank, NuBank, which has over 48 million users.

In the BRICs, Neobanks appear to be offer their customers convenience, 24-hour support and often reduced costs as they help serve the unbanked and underbanked.

Beating Ireland to the top spot is Brazil at #1 with 43% of the population having a Neobank account followed by India in the #2 spot with 26% of Indians using a digital-only bank.

Seon Technologies, which used data from Finder, reported that around 356,553,704 of India's populatuion could be Neobank account holders, putting them in first place as the country that uses digital banking the most. Meanwhile according to current population estimate for Braziln at 91,719,000, digitization of its economy has been accelerated by both the pandemic and popular Neobanks seeing their client base grow exponentially (a bit of a cause and effect observation). Brazil is also home to Latin America’s biggest Neobank, NuBank, which has over 48 million users.

In the BRICs, Neobanks appear to be offer their customers convenience, 24-hour support and often reduced costs as they help serve the unbanked and underbanked.

Figure 2

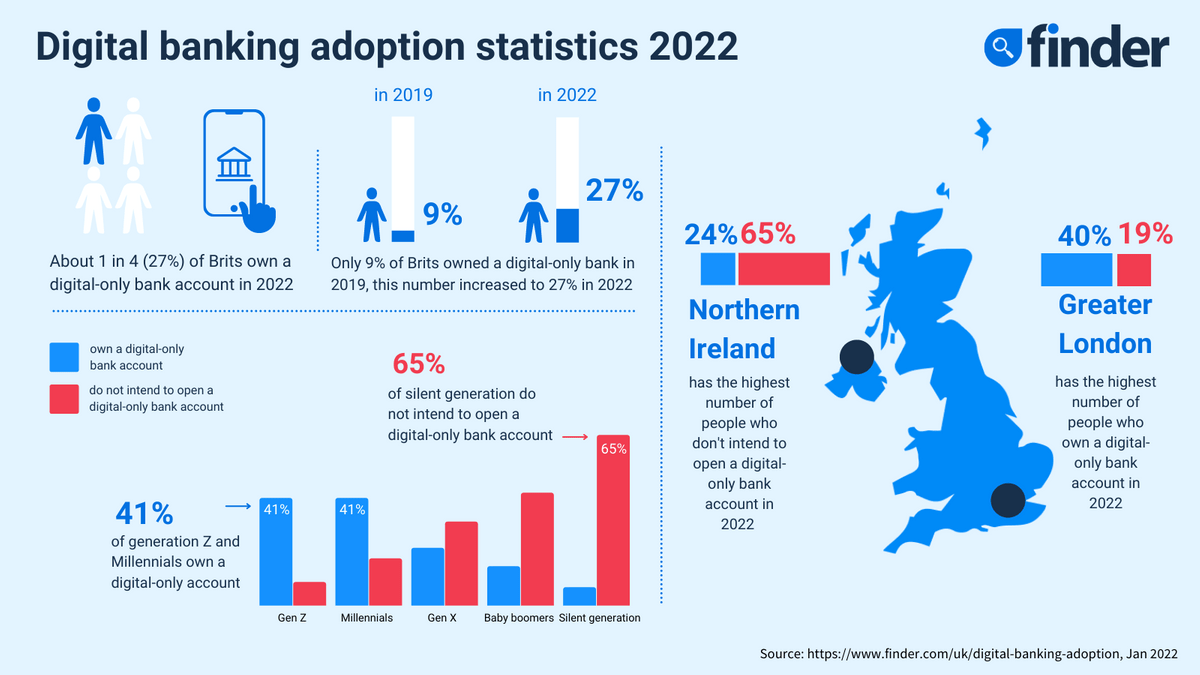

In January 2022, Finder released the above infographic on digital banking adoption in the UK. See Figure 2.

It reported at the time that about 1 in 4, in fact 27%, of Brits own a digital-only bank account. (1) It is hard to believe that the percentage has dropped in the period between January to July 2022; and (2) accordingly, why was the UK left off Finder's July 2022 update which showed that the top three spaces fell to Brazil, India and Ireland. At 27%, all things being equal, the UK at either the #2 (or #3) spot would have edged Ireland into 4th spot, right?

It reported at the time that about 1 in 4, in fact 27%, of Brits own a digital-only bank account. (1) It is hard to believe that the percentage has dropped in the period between January to July 2022; and (2) accordingly, why was the UK left off Finder's July 2022 update which showed that the top three spaces fell to Brazil, India and Ireland. At 27%, all things being equal, the UK at either the #2 (or #3) spot would have edged Ireland into 4th spot, right?

Which Neobanks have raised the most capital?

Figure 3

UK leads the way for Neobank capital raisings

Looking at the above graphic, sourced from the links above, the United Kingdom is the clear leader when it comes to the amount of capital raised by Neobanks. The collective total raised by UK Neobanks Wise, Revolut, Monzo, Starling Bank and OakNorth (as shown above) equates to USD17.9million. It is probably worth noting that if the USD figures for UK Neobanks were converted from GBP to USD, then these figures might need to be revisited given the slump of GBP against the USD this year.

The US comes 2nd to the UK based on the above figures at $11.5mn, with Brazil and Germany in 3rd and 4th place at $3.9mn and $1.7mn respectively.

The US comes 2nd to the UK based on the above figures at $11.5mn, with Brazil and Germany in 3rd and 4th place at $3.9mn and $1.7mn respectively.

Where Are Neobanks Being Adopted Faster?

Figure 4

Hats off to the Philippines, with around 13% of the population currently using Neobanks, Finder predicts (see link to source above) that by 2027 that figure will be around 33%, representing 33.3mn people. If correct that represents a 154% increase from 2022. Mexico, in position #2 is expected to see a 141% increase from 2022 - meaning that by 2027, 41% of Mexican residents (51.6mn) will likely be using Neobanking. Presently, it is estimated that 17% of people in Mexico currently hold a digital-only bank account.

No surprise to many of us in global fintech that Portugal makes the top 3 in this group. Around 14% of the Portuguese population currently uses a Neobank, and an estimated 32% will use Neobanking services by 2027. This indicates a 129% increase in Neobanking usage in the next five years.

No surprise to many of us in global fintech that Portugal makes the top 3 in this group. Around 14% of the Portuguese population currently uses a Neobank, and an estimated 32% will use Neobanking services by 2027. This indicates a 129% increase in Neobanking usage in the next five years.

Need a Neobank (emoney and payment) licence?

Check out Fintech Ireland's and CompliReg’s handy authorisation guides for e-money institutions and payment institutions at https://fintechireland.com/fintech-authorisations.html